Author|##BloFin

Compilation|##Ehan Wu said block Chain

The opinions expressed in this article are the author’s personal opinions and do not represent Wu Shuo’s views and positionsOriginal text:

https://medium.com/@BloFin_Official/whales-view-should-we-do-some-preparation-for-the-possible-rejection-of-spot-eth-etfs-f6b0173d598e

with spot Compared with Bitcoin ETFs, the negative impact of the PoS mechanism, price manipulation risks and securitization risks have significantly reduced the probability of approval of spot ETH ETFs. Fortunately, regardless of whether a spot ETH ETF is approved or not, the final outcome will not affect the ETH price breakout. However, as other competitors catch up, ETH's market share may struggle to increase further.

"Securitization Risk"Analysts’ concerns are not unfounded. Last year, the ETH futures ETF was approved, but with the US Securities and Exchange Commission (SEC) approving the listing of spot Bitcoin ETF, it seems that the SEC has developed a set of standards for reviewing cryptocurrency spot ETFs, namely "commodity tokens". These tokens are not It has security attributes and does not bring securitization risks.

There is no doubt that Bitcoin is one of the SEC’s “gold standards.”

●Bitcoin, like gold and other minerals, has limited reserves, is non-renewable and requires a specific cost to obtain.

●The Bitcoin network is stable and mature, and there will be no significant changes in the future due to factors such as consensus mechanism upgrades.

●Without experiencing an ICO (Initial Coin Offering) or any form of financing, its market has gradually formed based on buying and selling and transactions between users.

●The number of Bitcoin holders is large and dispersed, and the risk of price manipulation is relatively low.

However, for Ethereum, these standards do not seem to be met.

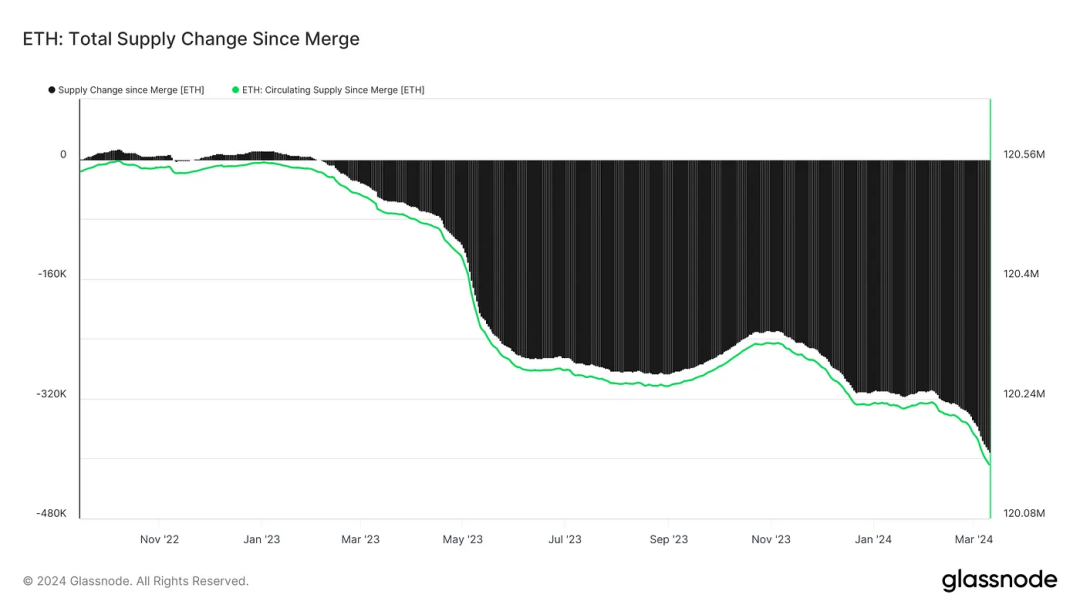

The new mechanism introduced by ETH 2.0 and subsequent upgrades will cause ETH to show a deflationary trend and reduce its total market stock. However, ETH will continue to be generated, and the theoretical total amount is unlimited. Its "inflation" and "deflation" are highly related to the activity level of its own network. During times of lower activity on the Ethereum network (such as July 2023), ETH "inflation" reappears.

Changes in Ethereum network activity (Source: Nansen)

Of course, one might argue that Ethereum Fang is a "renewable digital commodity" and a "crop" growing in the digital space. The Proof-of-Stake (PoS) mechanism is like sowing seeds and receiving a “harvest” after providing a “seed” of 32 ETH. However, holding crops does not have voting rights, while ETH holders under the PoS mechanism can obtain voting rights. The more ETH you hold, the more votes you hold and the more significant your impact will be on the future of the Ethereum network.

In addition, it is difficult to find a more reasonable explanation for the following series of standards, making ETH look more like a "commodity" than a "security".

●The Ethereum network is constantly being upgraded. After ETH futures were officially listed on CME, ETH underwent major changes in the second year. The consensus mechanism changed from PoW to PoS and the main network forked. With each upgrade, ETH becomes the “Ship of Theseus”: there are significant differences between ETH in March 2024 and ETH in March 2021.

●Ethereum conducted an ICO in 2014. The ICO record makes ETH itself subject to a certain "security risk," as the U.S. Securities and Exchange Commission and financial institutions in other countries have stated that "ICO tokens may be considered securities." The SEC may consider assets with disputed attributes more carefully.

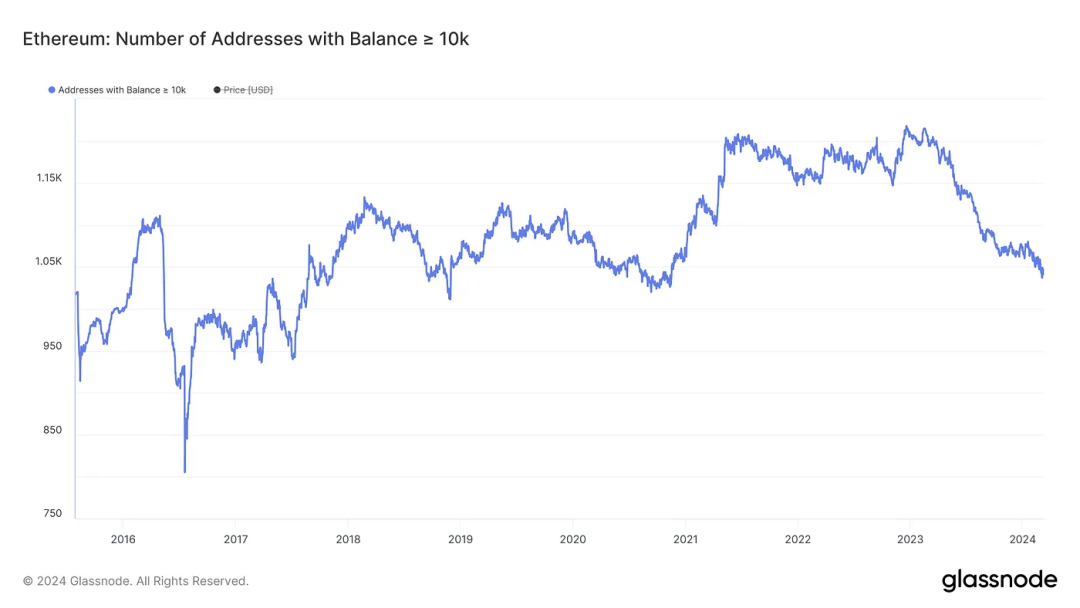

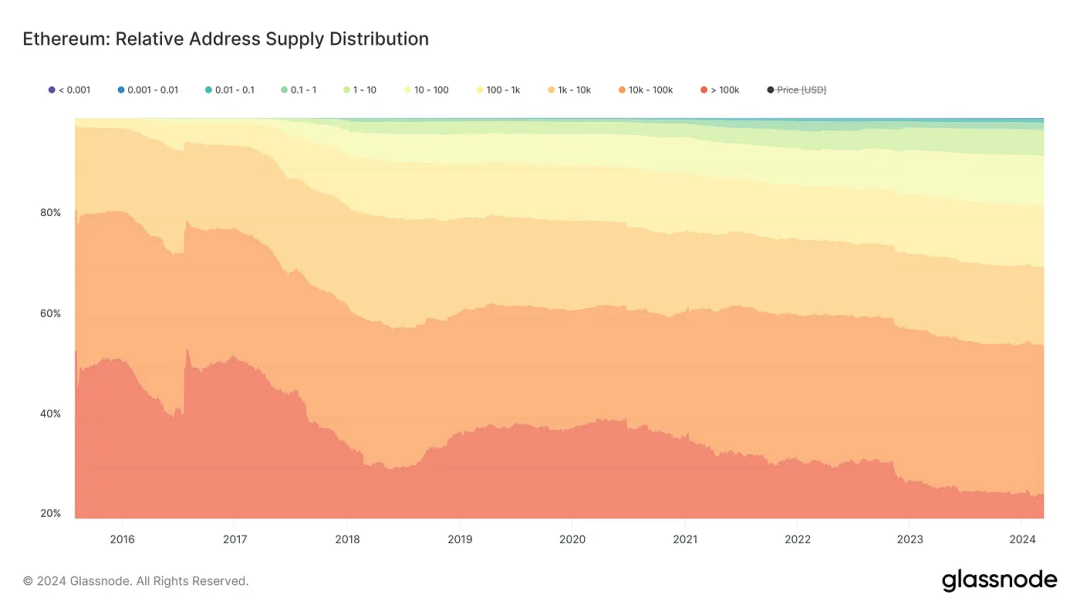

●According to Glassnode statistics, nearly 55% of the ETH supply (approximately 66 million tokens) is held by 1,041 addresses, with an average balance of more than 10,000 ETH. In comparison, retail traders account for less than 45% of the ETH supply. At the same time, considering that under the PoS mechanism, token holdings are almost directly related to voting rights, the holders of these 1,041 addresses can have a significant impact on the upgrade and operation of the ETH network.

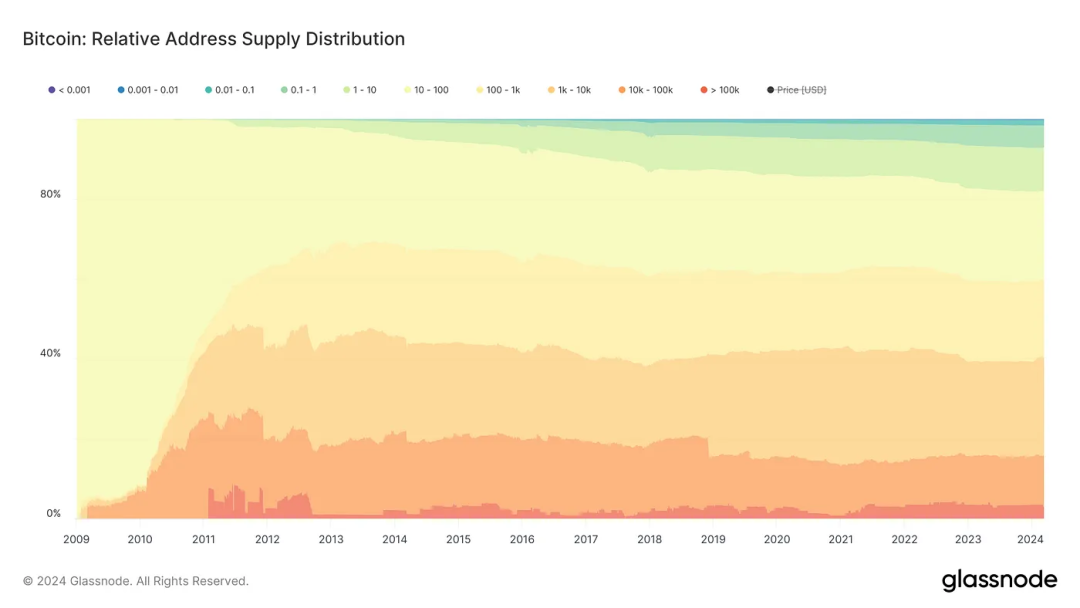

In contrast, BTC holders have no voting rights and will not have a significant impact on the operation of the BTC network. Since 2009, the distribution of BTC holders has become quite natural and even: as of March 2024, whales holding more than 1,000 BTC only own about 40% of the BTC supply, and the number of whale addresses has reached 2,100 , which makes the possibility of BTC price manipulation significantly lower than that of ETH.

#The SEC has not yet begun to downplay its concerns about the risks that may arise from the ETH PoS mechanism. In public documents, the SEC expressed concern about the risks that may arise from the ETH PoS mechanism:

"...specific characteristics of Ethereum and its ecosystem, including its proof-of-stake consensus mechanism and the presence of a small number of individuals or entities Are there unique concerns that make Ethereum vulnerable to fraud and manipulation due to its concentration of control or influence?”

Overall, while hoping for a spot ETH ETF to be approved due to “securitization risks,” one must also be prepared for a rejection from the SEC.

Compared to the market when the spot Bitcoin ETF was approved, it seems that spot whales and derivatives traders were not sufficiently expecting and preparing for the approval of the spot ETH ETF.

From the perspective of on-chain data, although the quarterly selling behavior of miners has had a certain impact on the statistics, the number of addresses holding balances of more than 100 BTC has shown a significant upward trend since May 2023. . The impact of miner selling on address numbers was significantly weaker compared to Q1 2022 and H1 2023, meaning many spot whales bought large amounts of BTC during this period, and spot BTC ETFs were subsequently approved.

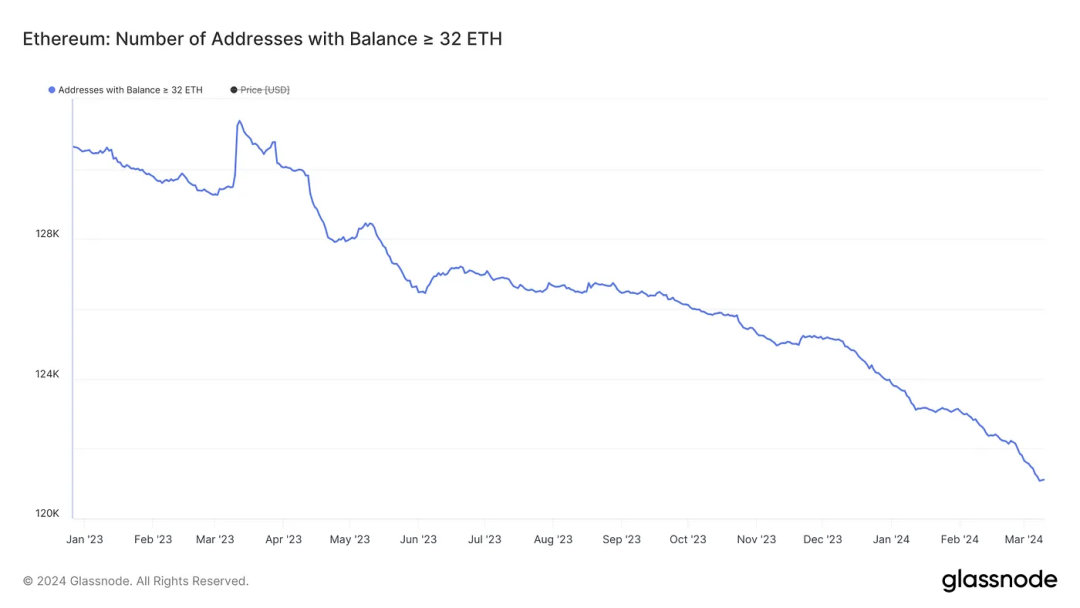

But no similar signs were found on ETH. Even with relatively loose standards, the number of addresses with balances above 32 ETH has continued to decrease since January 2023, and the hype in the spot ETH ETF has not had a noticeable impact on the downward trend. Instead, the downward trend has accelerated.

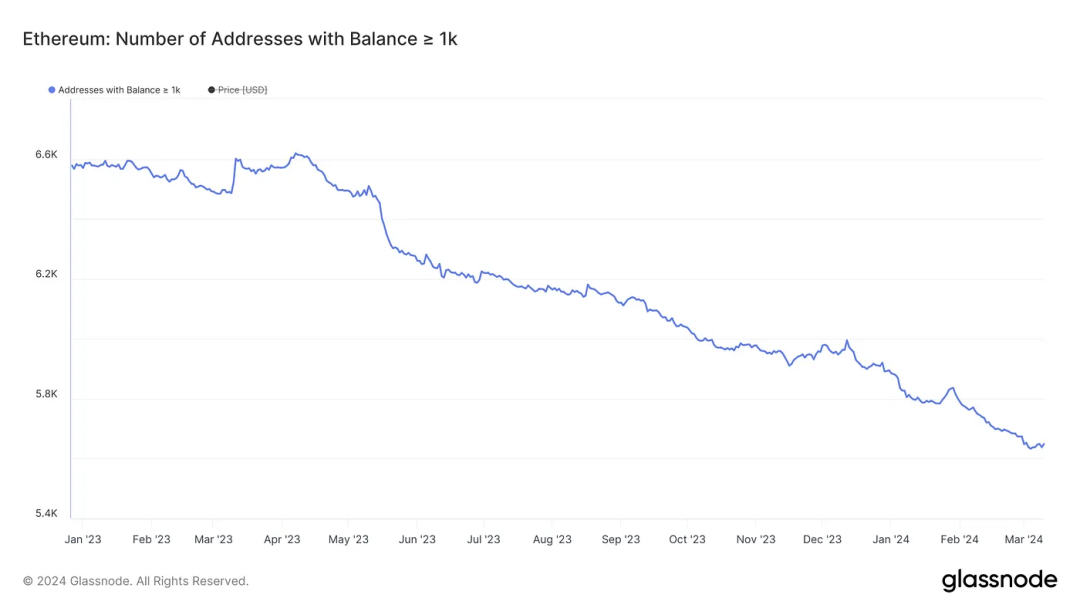

The same conclusion can be drawn if only addresses with balances over 1000 ETH are considered. Whales appear to be taking advantage of speculation and optimism by selling ETH for profit.

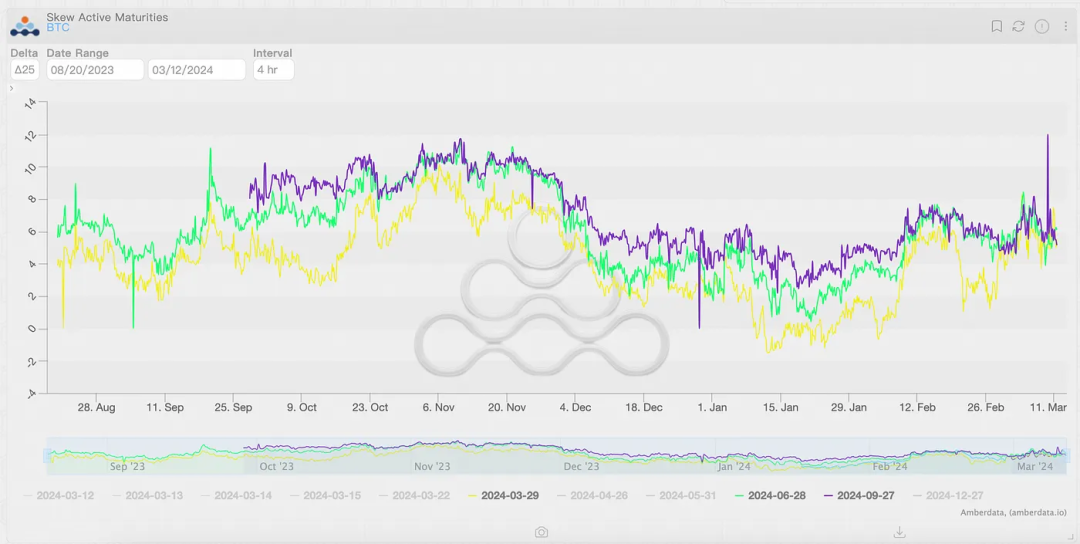

There are also some possible clues in the options market. Following the announcement of the spot BTC ETF application, far-month option skew for both BTC and ETH increased significantly, peaking in November 2023. In contrast, the spot ETH ETF filing received little attention from options traders upon its announcement. The increase in bullish price sentiment and the increase in far-month skewness in February are more likely to be affected by the return of liquidity.

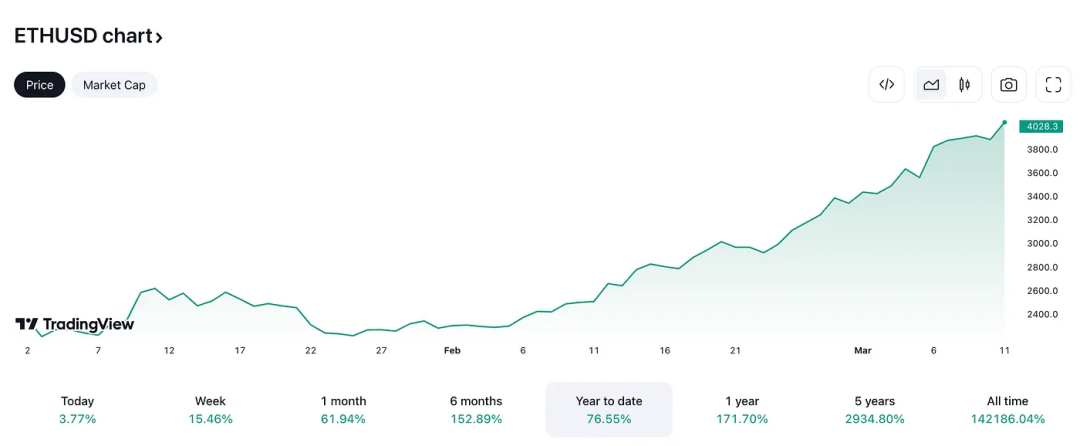

There is no doubt that the approval of spot ETFs will provide sufficient support for the price performance of BTC and ETH. After the spot ETF was approved, the additional liquidity support in the U.S. stock market drove the price of BTC to rise by more than 71% year-to-date, with the price of BTC once exceeding $72,000, a record high.

It is worth noting that although the performance of ETH in terms of exchange rate is relatively weaker than that of BTC, in terms of price increase, the price performance of ETH is not inferior to that of BTC. Even the year-to-date increase is slightly better than that of BTC.

#ETH’s surprisingly good performance depends on a variety of factors. On the one hand, the inertia of investors in the crypto market prompts them to sell BTC and buy ETH when BTC prices rise significantly, "bridging" cash liquidity stored in BTC to cryptocurrencies such as ETH. At the same time, the rapid return of cash liquidity provides more support for the price of ETH, and ETH's relatively high volatility brings higher growth potential.

Therefore, as more cash liquidity flows into the crypto market, in the medium to long term, ETH price increases are expected and already priced in the derivatives market. The continued positive skewness of far-month ETH options is the best reflection of investors’ bullish sentiment. It is only a matter of time before the price of ETH reaches new highs.

The approval of spot ETFs will only speed up the above process, but it doesn’t matter if it is not approved. The price of ETH may see some volatility or even a significant correction. But in a bull market environment, the gap caused by the decline will be quickly filled, and the upward trend of ETH prices will not fundamentally change.

It is worth noting that when spot ETFs cannot be approved, ETH needs to face other competitors within the crypto market. SOL has performed relatively better than BTC over the past six months, and other public chain tokens are also poised to make a move.

Although ETH’s leading position will not be challenged for the time being, other competitors will undoubtedly take away more cash liquidity that originally belonged to ETH. As central banks around the world have adopted relatively stable monetary policies, the return of liquidity to the crypto market will be a “relatively slow and steady” process. Therefore, competition for existing cash liquidity will be one of the main challenges for ETH.

The above is the detailed content of Should we prepare for Ethereum spot ETF rejection?. For more information, please follow other related articles on the PHP Chinese website!

![[Web front-end] Node.js quick start](https://img.php.cn/upload/course/000/000/067/662b5d34ba7c0227.png)