Base DEX Faucet: Aerodrome VS Curve

The Velodrome model is inspired by veCRV and aims to achieve superior consistency among the three key participants of DEX, including liquidity providers (LPs), token holders, and projects that require liquidity. However, many players in the DeFi space still do not fully understand the underlying reasons. By reading this article in-depth, you will be able to get out of this dilemma and get to the bottom of it.

Today we will discuss Velodrome/Aerodrome, a real success story in the field of DeFi. This article will compare the two models and explain how Velodrome improves on the veCRV model and what significant impact these small differences have.

First, let me make something clear: To understand what follows, everyone needs to realize that a DEX has two core components:

1. The liquidity structure it provides (e.g. x*y=k, stableswap, CL, stableswap-NG, curve V2, etc.)

2. Incentive model, for DEX, this is synonymous with its tokenomics.

This article focuses on the latter, the core of Velodrome’s innovation. This article assumes you have a basic understanding of Curve’s veCRV token economics.

A/ veCRV / veVELO Fee collection and distribution

Fee collection and redistribution are the keys to decentralized exchanges. Simple is often the better option in this regard, as leaders like Uniswap still adhere to an extremely simple but efficient model that attributes 100% of fees directly to liquidity providers.

With the launch of the CRV token in August 2020, Curve explored an alternative path where 50% of the fees collected on a given trading pair went to liquidity providers and the remaining 50% went to the “DAO ” (management fee), that is, veCRV holders. Curve introduces the concept of "liquidity metering" where locked token holders (veCRV) can direct CRV emissions to be received by liquidity providers, creating a new incentive strategy.

Launched at the end of May 2022, Velodrome explores a new way of forking, inspired by Solidly, a previous project that iterated on the Curve model. In Velodrome, LPs do not charge fees on trading pairs that provide liquidity, but are incentivized through emission rewards. This innovative approach has attracted widespread attention in the blockchain community, bringing a new way of thinking to the DeFi ecosystem. The launch of Velodrome provides more incentives and opportunities for participants, while also echoing the core concept of decentralized finance. This emission reward-based model provides participants with more flexibility and opportunities, incentivizing them to participate more actively in liquidity provision and trading activities

The key difference between veCRV and veVELO is their How fees collected at the DEX/DAO level are handled. We noticed clear differences in the amount of fees collected and the distribution model.

Let’s dive into the nuances of this topic: they are the key to understanding the pros and cons of each mode.

A.1/ Amount of fee distribution: VELO = 2 x Curve

Curve and Velodrome follow the same basic logic: every week, a certain number of CRV/VELO tokens are issued and distributed to liquidity providers. Each pool has a meter associated with it that veCRV/veVELO holders can vote, and the weekly budget allocation follows a "meter vote" ratio: if a meter receives 1% of the total veCRV/veVELO votes, then that week 1% of all issuance generated will be directed to this currency pair.

These issuances are essentially the primary cost of a DEX: the price paid to attract and retain liquidity. What matters then is the other side of the ledger – revenue: in our case, fees collected.

On Curve, revenue comes from a “management fee” on each pool, which is usually set at 50%. This means that the fees charged on a given pool are split equally between LP and DAO/veCRV holders.

#Curve revenue overview: light blue is management fees, yellow is fees paid to LPs, dark blue is revenue from crvUSD stablecoin - Source: curvemonitor.com

On Velodrome, it's simple: liquidity providers don't get fees charged on the trading pairs they supply in the pool; they only get incentives through $VELO emissions, which means DAO/veVELO holds The investor receives 100% of the fees generated on DEX.

While this core difference already has a huge impact, the next difference is even more meaningful when it comes to how these fees are allocated to veCRV/veVELO holders.

A.2/ Fee Allocation Model: A Fairer, More Efficient Approach

Curve adopts a model that can be described as a fee-levelling system: veCRV holders receive only Depends on the amount of veCRV they hold. Stripping away too many technical details, these fees are charged in the various tokens involved in the pool (e.g. 3pool’s USDC/USDT/DAI), which are harvested, exchanged for 3pool LP tokens every week, and then made available for veCRV to hold Claimable - As you can see, this means that some kind of infrastructure is required to operate, the cost of which increases with the number of pools on Curve DEX.

On the other hand, Velodrome offers a superior model in all dimensions as it achieves better consistency among DEX/LP/token holders without requiring any infrastructure. Let's see how it's done.

Simply put, Velodrome connects metered voting activities with fee distribution. Here, the amount of veVELO a holder owns matters, but even more important is which pool they voted for, as voters will only receive the fees charged on the trading pair they voted for. They charge per-pool fees (i.e. voters of the ETH/USDC pool receive ETH and USDC), which means the required infrastructure is easier to manage.

Velodrome ties fee distribution to metered voting activity: veVELO holders only receive fees charged on the pool they voted for, paid out once a week in the currency pair of the original pool. This better aligns veVELO holders with the best interests of Velodrome as a DEX compared to Curve.

This simple switch creates an interesting voting flywheel. High-volume trading pairs charge large fees, meaning there is a high incentive for voters. This results in a lot of votes > directing reasonable issuance to the pair > attracting more liquidity providers > taking on more trading volume. until a balance point is reached. This means that a large number of currency pairs can be self-sustaining without requiring bribes or seeking whale voters, which is not the case on Curve.

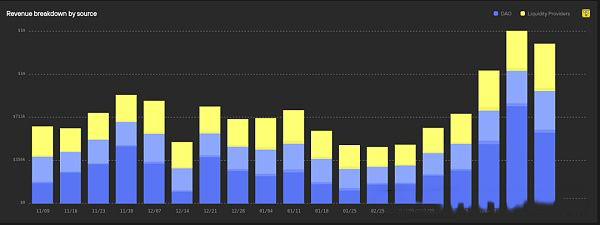

Velodrome Revenue Overview - Source: 0xkhmer Dashboard

Aerodrome Revenue Overview - Source: 0xkhmer Dashboard

A.3/ Meaning in practice

Now, let us illustrate by considering the case of a veCRV/veVELO voter who decides to vote for a transaction with the smallest transaction volume (this is a common situation) Trading pairs vote.

On Curve:

1. A significant veCRV holder votes for a pool that handles a small volume compared to its TVL, either to collect a bribe or because he wants to Supports the tokens involved in the pool.

2. His voting activity is harmful to Curve as a DEX because he directs issuance to unnecessary places.

3. He receives the same amount of 3CRV as a more Curve-inclined voter, who has an equal amount of veCRV packets, trying to direct incentives toward votes that maximize transaction volume.

Now on Velodrome:

1. A significant veVELO holder votes for a pool that handles a small volume compared to its TVL, either to collect a bribe or because he Want to support the tokens involved in the pool.

2. His voting campaign is harmful to Velodrome as a DEX because he directs issuance to unnecessary places.

3. The amount of fees he receives is very small because the pool he votes for handles very small transaction volumes.

The same is true for voting for a high volume pool that a DEX is interested in:

• On Curve, this DEX-aligned voter will receive the same tokens as any holder of Coin voters have the same amount of 3CRV.

•On Velodrome, this DEX-aligned voter will be well rewarded because he will be the majority voter on a high-volume pair: the ideal situation to maximize earned fees.

In both respects, bribes are paid to voters and may result in votes being directed to pools that are not optimal in terms of handling transaction volume. On Curve, however, there is no penalty for doing so. On Velodrome, bribers of these pools compete with high volume pools that offer attractive APRs, with or without bribes.

Look at it from another perspective: on Curve, the cost of a bribe only depends on the value of the CRV issued. On Velodrome, the base price a project must pay is determined by the total bribe fees charged by other pools. This means that high volume pools drive up the cost of bribery, providing another incentive within the flywheel.

Understanding the above means understanding the core differences between the Curve and Velodrome models. However, for a complete understanding, many more elements must be considered. Let us discuss LP boost now.

B/ LP Boost and its impact on the ecosystem

LP boost, to put it simply, is a function unique to Curve. Many protocols that adopt veCRV tokenomics, such as Balancer and its veBAL, also use this feature. It enables veCRV holders to earn more CRV rewards based on multiple factors, including their veCRV holdings and the size of their various LPs. Therefore, with appropriate veCRV ownership, LPs can receive an "LP Boost" of up to 2.5x the base issuance rate.

B.1/ LP boost explanation

In order to get the maximum boost, up to 2.5 times, the following must be done:

1. As much as possible Hold veCRV.

2. Hold LP positions in as many pools as possible.

3. Have proportional/balanced TVL across these different pools.

Simply put, LP boost is a tough game from the beginning. It is not intended to benefit individual veCRV holders relative to their LPs, but rather to attract new protocols. With protocols like Convex, they are able to consistently achieve 1 2 3 all the time. Convex's growth is not a success story; it's by design (Curve's design). Without Convex, another similar protocol would own the majority of the veCRV supply. We observed similar patterns in other protocols employing LP boost: Balancer has Aura. Convex and Aura control over 50% of the veCRV/veBAL supply.

Velodrome and Aerodrome completely avoid the possibility of new protocols gobbling up supply by not having any boosting mechanisms. As we have seen with Curve, Convex came along and took the majority of the supply; now all LPs are getting boost and no one is benefiting from any disproportionate amount of CRV. The system has converged to the point where everyone gets about the same effective boost. In Velodrome/Aerodrome, there is no Boost, as the future result will be that the LP gets the same effective boost. Another fact is that since Convex owns the majority of locked CRV, they control the future governance of CRV.

B.2/ Consequences of LP Boost

The existence of LP-boost requires a Convex-like layer on top of DEX; this is unavoidable. At this point, some may be thinking: "So you have a protocol that eats up most of your issuances and locks them up forever; what's the problem?"

The answer is simple: it's just design inefficiencies because these meta-layers provide functionality that can be provided at the base level (by the DEX itself) in a simpler way and at no cost.

Curve requires Convex and the Bribery Market: Votium, Warden and Hidden Hands. But automatic compounding/voting proxy managers are also needed: Airforce Union, Concentrator, etc. You'll end up seeing dozens of protocols charging some fees here and there to provide what Velodrome is able to package natively. This makes the user experience more complex, and users must understand these protocols and their subtleties to get the most out of Curve.

Remember when we discussed fee allocation we mentioned that Curve requires more intensive infrastructure to operate? Well, imagine the chaos on the back end of the veCRV LP boost. There's a reason why Curve and Balancer took so long to launch on the new L2, often with only partial functionality (e.g. no LP boost, surprise surprise).

Seamless expansion—beyond what Curve has to offer:

On Velodrome, the bribe market is built-in: projects can publish their bribes directly on the Velodrome front-end, and voters can View available bribes and vote in the same place.

Velodrome Relays

They start with quality of experience/Gas saving upgrades such as Auto Max Lock, saving savings for lockers who want to stay max locked to maximize their meter vote volume Take the hassle out of manual operations, to broader features like Relay, a veVELO location management system.

This is a tool for projects that use Velodrome to grow liquidity on their trading pairs. It enables them to set up their own voting and bribery strategies and have them implemented automatically: no more weekly submissions of transactions. Relay has an additional benefit, as the currently available strategy is a veVELO-maxi strategy, which compounds all collected fees and bribes into VELO and relocks them to maximize voting power: it creates a sizable VELO pool, directly Tied to fees allocated by the exchange. Nearly 1/5 of veVELO is already there.

As Relay’s functionality matures, more strategies will become available to its users, including some that compound all earned fees and bribes into veVELO. Or a strategy to automatically claim ETH or USDC. This is very convenient for veVELO holders who don’t particularly want to support a project.

veNFT: Tokenization of Positions

Velodrome also includes other neat innovations, such as the still underrated veNFT: on Curve, veCRV are non-transferable, making their management pain. Velodrome achieves the same consistency but allows for transferability: veVELO positions are represented by veNFT and can be transferred. There is no way to redeem a given veNFT for VELO native currency other than waiting for the lock to expire. However, it simplifies the management of such a position by allowing transfers. Additionally, there is an OTC market for veVELO veNFT where holders can sell their positions at a discount compared to the value of VELO’s native currency.

A deep understanding of the nature of the game

Exchanges like Curve or Velodrome are a special type of product in the DeFi landscape. In regular business terms, they can be described as B2B2C: business to business to consumer. They are B2B because their first customers are other projects - various protocols looking for liquidity. If they successfully serve this market, the projects they bootstrap into their DEXs will do the B2C job for them as their liquidity pools provide opportunities for their respective token holders.

In this regard, I feel like Curve has completely failed. With its pyramid structure of solutions nested within each other, Curve is particularly unfriendly to project access. Do they want a bribe? Ok, decide between veCRV or vlCVX Bribe, Votium, Warden or StakeDAO on Bribe.crv. Do they want to manage their own CRV? Ok, just choose between veCRV, aCRV, cvxCRV, sdCRV, vlCVX, uCRV and more. While this variety of options may be exciting for Curve enthusiasts, in my opinion it becomes a liability on the B2B side.

The Velodrome experience, by contrast, is seamless: everything happens in one place, every option is clear, and there's no need to compare between a half-dozen obscure and sometimes misleading choices. Combined with the previously discussed features of the veCRV game, specifically the LP boost, it makes the Curve ecosystem particularly unfriendly to new entrants: who would want to enter a competition where three years after it started the interests are still skewed towards the first entrants?

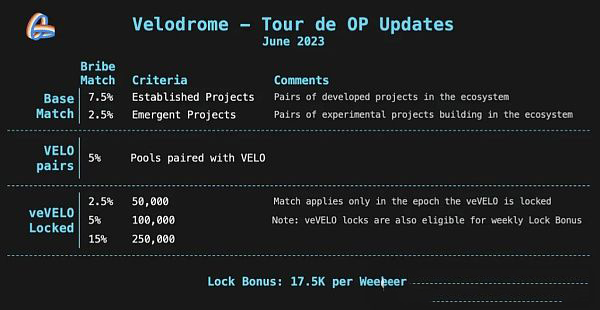

Additionally, Velodrome’s BD efforts are significant; the team helps new projects onboard extensively and has designed several plans to make the experience for new entrants as simple as possible and compelling, which all come under the "Tour de OP" umbrella and include bribery matching programs, locked rewards, and voting enhancements.

Summary

As you may have seen, Velodrome and Aerodrome have attracted a lot of attention recently due to the rally of their tokens: I think it is well deserved. The launch of Velodrome’s implementation of centralized liquidity Slipstream will increase the transaction volume processed per unit of TVL, unlocking the next growth stage of the flywheel. Aerodrome, Velodrome’s offshoot on the Base network, has seen phenomenal growth since its launch six months ago, further proving the viability of this model.

In the long term, the Velodrome team began to refer to Velo as "MetaDEX", implying that Velodrome is becoming not just Optimism, but the basic liquidity center of the entire superchain (Superchain): all built on the OP stack on the chain.

Time will tell, but Velodrome has had great success with Optimism, so properly managing a cross-chain DEX will be a game changer. This is especially true considering Curve and Balancer failed there - not because they didn't try, but because their complex infrastructure and LP boost made cross-chain deployment painful (like AuraFinance distributing AURA on a chain with no liquidity ).

PS: I'm talking about the DEX part of the product suite here, which is the full range of products for Velodrome, but not for Curve, which now has crvUSD and Llamalend. Still, even including crvUSD, Aerodrome now collects and distributes more fees than Curve, all on one chain compared to Curve’s 13. While Curve-DEX has been underperforming for a while, the team has proven its ability to innovate and bounce back multiple times. crvUSD has surpassed Curve-DEX in revenue, who knows what Llamalend can achieve.

The game continues: Let’s wait and see.

The above is the detailed content of Base DEX Faucet: Aerodrome VS Curve. For more information, please follow other related articles on the PHP Chinese website!

Hot AI Tools

Undresser.AI Undress

AI-powered app for creating realistic nude photos

AI Clothes Remover

Online AI tool for removing clothes from photos.

Undress AI Tool

Undress images for free

Clothoff.io

AI clothes remover

AI Hentai Generator

Generate AI Hentai for free.

Hot Article

Hot Tools

Notepad++7.3.1

Easy-to-use and free code editor

SublimeText3 Chinese version

Chinese version, very easy to use

Zend Studio 13.0.1

Powerful PHP integrated development environment

Dreamweaver CS6

Visual web development tools

SublimeText3 Mac version

God-level code editing software (SublimeText3)

Hot Topics

1377

1377

52

52

okx Ouyi Exchange web version enter link click to enter

Mar 31, 2025 pm 06:21 PM

okx Ouyi Exchange web version enter link click to enter

Mar 31, 2025 pm 06:21 PM

1. Enter the web version of okx Euyi Exchange ☜☜☜☜☜☜ Click to save 2. Click the link of okx Euyi Exchange app ☜☜☜☜ Click to save 3. After entering the official website, the clear interface provides a login and registration portal. Users can choose to log in to an existing account or register a new account according to their own situation. Whether it is viewing real-time market conditions, conducting transactions, or managing assets, the OKX web version provides a simple and smooth operating experience, suitable for beginners and veterans. Visit OKX official website now for easy experience

What is Ouyi for? What is Ouyi

Apr 01, 2025 pm 03:18 PM

What is Ouyi for? What is Ouyi

Apr 01, 2025 pm 03:18 PM

OKX is a global digital asset trading platform. Its main functions include: 1. Buying and selling digital assets (spot trading), 2. Trading between digital assets, 3. Providing market conditions and data, 4. Providing diversified trading products (such as derivatives), 5. Providing asset value-added services, 6. Convenient asset management.

gate.io latest registration tutorial for beginners

Mar 31, 2025 pm 11:12 PM

gate.io latest registration tutorial for beginners

Mar 31, 2025 pm 11:12 PM

This article provides newbies with detailed Gate.io registration tutorials, guiding them to gradually complete the registration process, including accessing the official website, filling in information, identity verification, etc., and emphasizes the security settings after registration. In addition, the article also mentioned other exchanges such as Binance, Ouyi and Sesame Open Door. It is recommended that novices choose the right platform according to their own needs, and remind readers that digital asset investment is risky and should invest rationally.

The latest registration tutorial for gate.io web version

Mar 31, 2025 pm 11:15 PM

The latest registration tutorial for gate.io web version

Mar 31, 2025 pm 11:15 PM

This article provides a detailed Gate.io web version latest registration tutorial to help users easily get started with digital asset trading. The tutorial covers every step from accessing the official website to completing registration, and emphasizes security settings after registration. The article also briefly introduces other trading platforms such as Binance, Ouyi and Sesame Open Door. It is recommended that users choose the right platform according to their own needs and pay attention to investment risks.

How to roll positions in digital currency? What are the digital currency rolling platforms?

Mar 31, 2025 pm 07:36 PM

How to roll positions in digital currency? What are the digital currency rolling platforms?

Mar 31, 2025 pm 07:36 PM

Digital currency rolling positions is an investment strategy that uses lending to amplify trading leverage to increase returns. This article explains the digital currency rolling process in detail, including key steps such as selecting trading platforms that support rolling (such as Binance, OKEx, gate.io, Huobi, Bybit, etc.), opening a leverage account, setting a leverage multiple, borrowing funds for trading, and real-time monitoring of the market and adjusting positions or adding margin to avoid liquidation. However, rolling position trading is extremely risky, and investors need to operate with caution and formulate complete risk management strategies. To learn more about digital currency rolling tips, please continue reading.

ok official portal web version ok exchange official web version login portal

Mar 31, 2025 pm 06:24 PM

ok official portal web version ok exchange official web version login portal

Mar 31, 2025 pm 06:24 PM

This article details how to use the official web version of OK exchange to log in. Users only need to search for "OK Exchange Official Web Version" in their browser, click the login button in the upper right corner after entering the official website, and enter the user name and password to log in. Registered users can easily manage assets, conduct transactions, deposit and withdraw funds, etc. The official website interface is simple and easy to use, and provides complete customer service support to ensure that users have a smooth digital asset trading experience. What are you waiting for? Visit the official website of OK Exchange now to start your digital asset journey!

How to calculate the transaction fee of gate.io trading platform?

Mar 31, 2025 pm 09:15 PM

How to calculate the transaction fee of gate.io trading platform?

Mar 31, 2025 pm 09:15 PM

The handling fees of the Gate.io trading platform vary according to factors such as transaction type, transaction pair, and user VIP level. The default fee rate for spot trading is 0.15% (VIP0 level, Maker and Taker), but the VIP level will be adjusted based on the user's 30-day trading volume and GT position. The higher the level, the lower the fee rate will be. It supports GT platform coin deduction, and you can enjoy a minimum discount of 55% off. The default rate for contract transactions is Maker 0.02%, Taker 0.05% (VIP0 level), which is also affected by VIP level, and different contract types and leverages

What are the recommended websites for virtual currency app software?

Mar 31, 2025 pm 09:06 PM

What are the recommended websites for virtual currency app software?

Mar 31, 2025 pm 09:06 PM

This article recommends ten well-known virtual currency-related APP recommendation websites, including Binance Academy, OKX Learn, CoinGecko, CryptoSlate, CoinDesk, Investopedia, CoinMarketCap, Huobi University, Coinbase Learn and CryptoCompare. These websites not only provide information such as virtual currency market data, price trend analysis, etc., but also provide rich learning resources, including basic blockchain knowledge, trading strategies, and tutorials and reviews of various trading platform APPs, helping users better understand and make use of them