Original title: The OnChain Report: 2024 Q1

Original author: QuickNode & Artemis

Original compilation: Felix, PANews

Key points:

StablecoinActivitySurge: Stablecoin user activity surged 42% month-on-month due to a combination of factors including the approval and listing of spot Bitcoin ETFs, April’s Bitcoin halving, hyperinflationary fiat currency outflows, and the resurgence of DeFi. %.

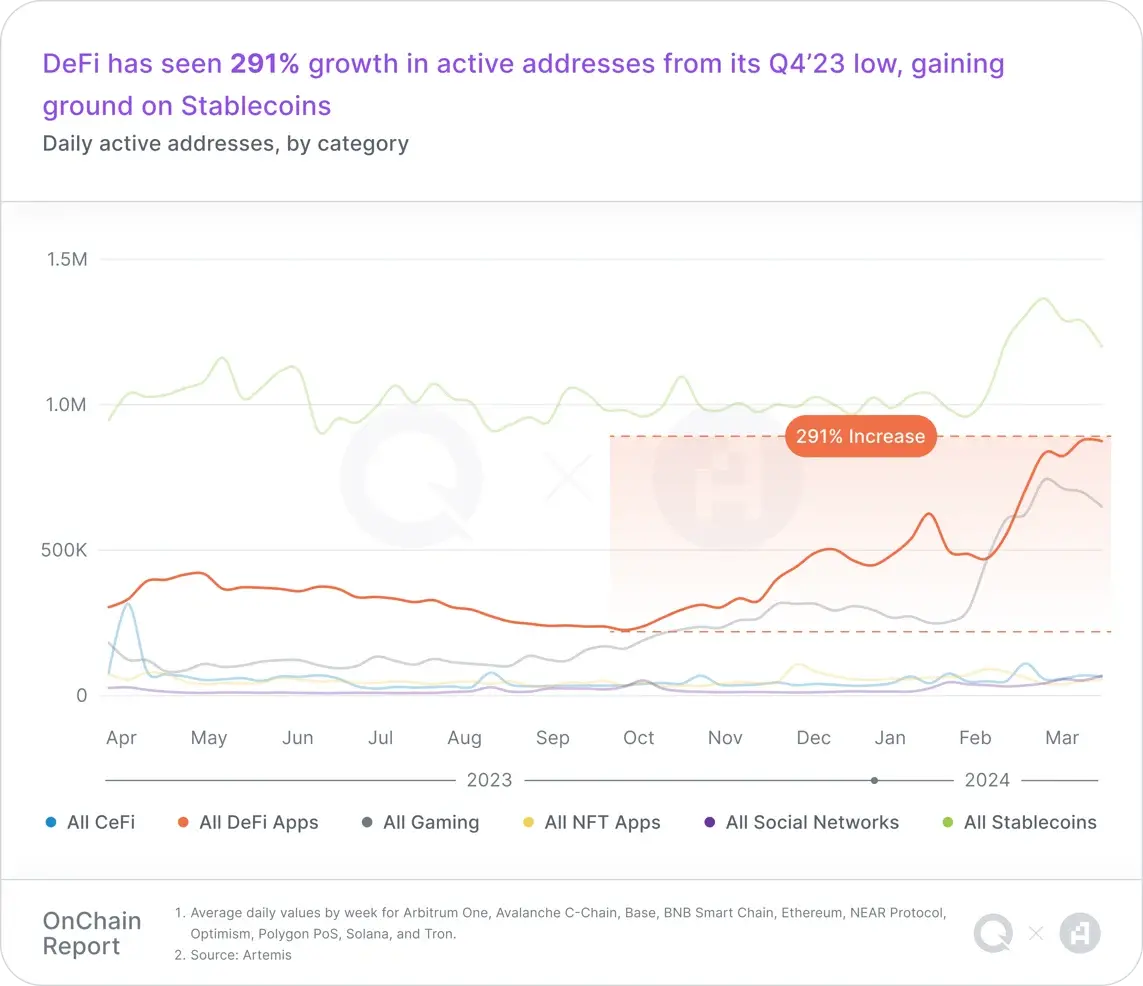

Reigniting the “DeFi Summer”: In the first quarter of 2024, DeFi entered a new era characterized by optimism, risk awareness, and sophisticated innovation . DeFi user activity increased by 291% month-on-month, and the market rekindled hopes for a "DeFi Summer".

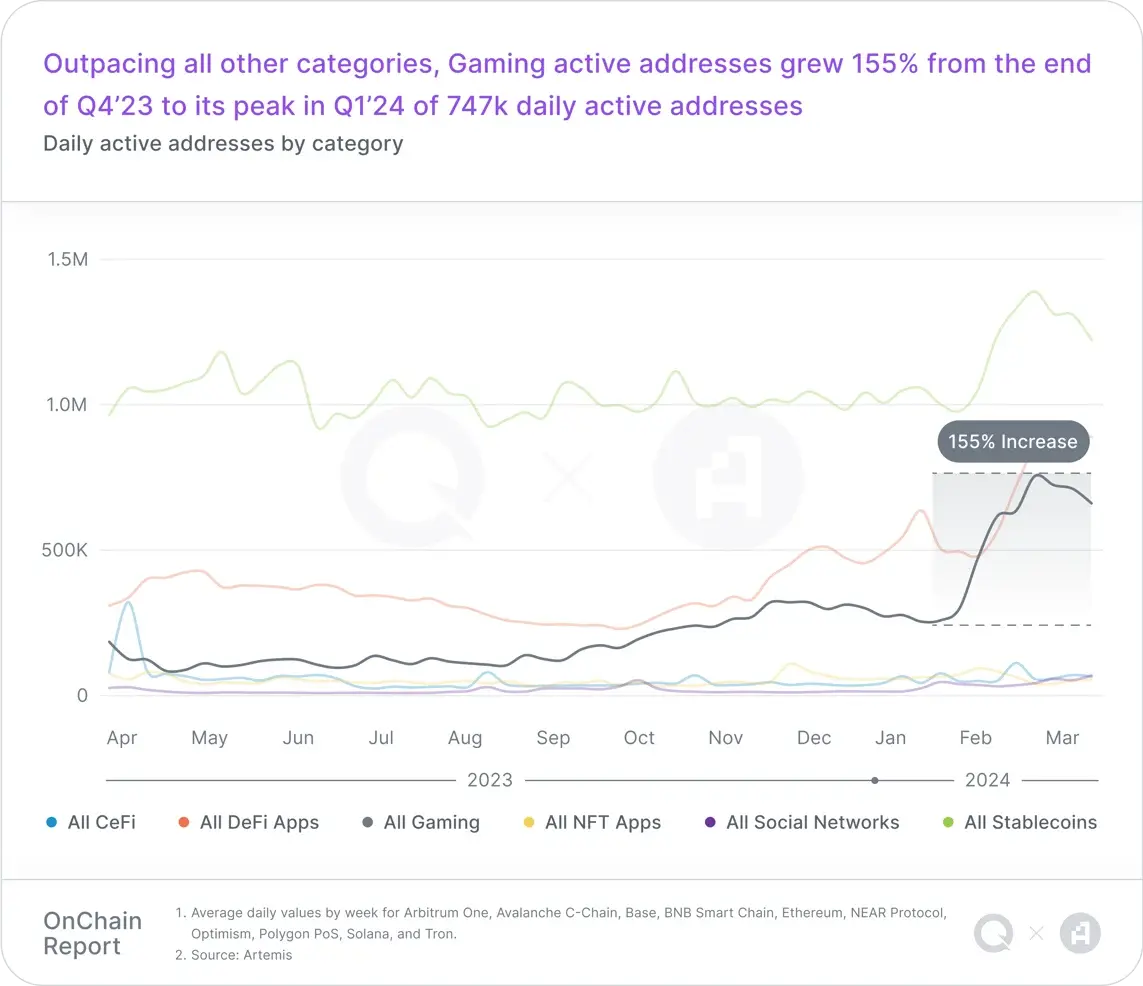

#Web3 gaming is heating up: The number of active addresses increased by 155% month-on-month, and the significant increase in player participation demonstrates Web3’s ability to attract and retain an ever-growing number of players. ability.

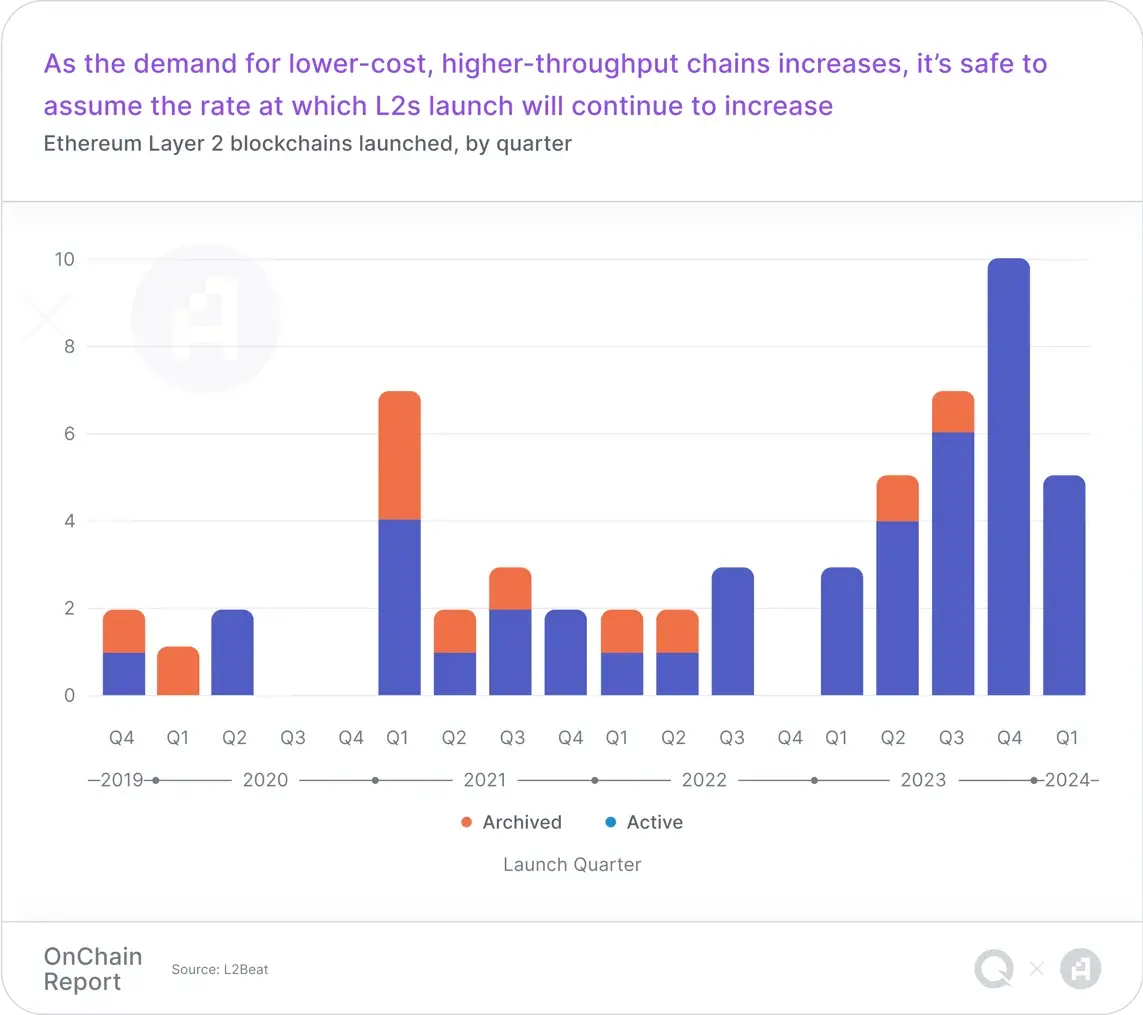

Layer2s Rapid Scaling: The rapid scaling of Layer2 marks a critical step forward in Web3 scaling over the past 6 months. In particular, the substantial increase in TVL on platforms such as Base shows that the market still has interest in expanding on-chain liquidity.

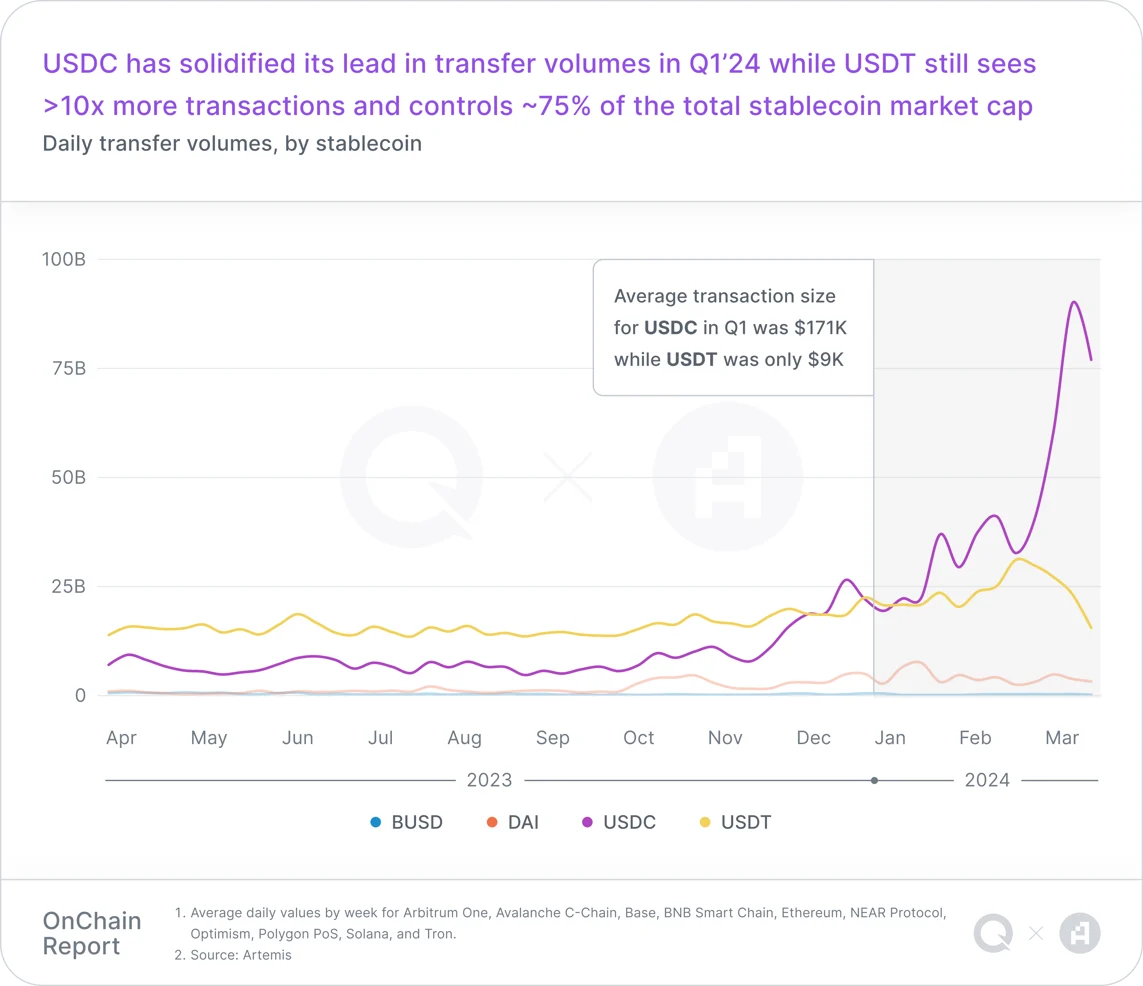

has the most active addresses for five consecutive quarters, accounting for more than 41% of all daily active addresses (DAA). USDT continues to dominate stablecoins, accounting for about 75% of the total market value of stablecoins. In the first quarter of 2024, the market value of USDT exceeded US$100 billion for the first time.

Although USDT processed more than 10 times the number of transactions than USDC in Q1’24, USDC leads the way in terms of transaction volume and average transaction size.

The number of daily active addresses in DeFi increased by 291% month-on-month in the first quarter. This growth represents a resurgence in capital inflows and the emergence of new revenue-generating protocols that fuel increased user activity.

DeFi has truly entered a new era in the first quarter of 2024, with a huge increase in developer and user activity, especially Solana and the Base network. Staking, liquidity staking, re-staking, and liquidity re-staking have all been catalysts for DeFi’s recent explosive growth, which explains why staking now accounts for a large portion of DeFi TVL.

While stablecoins still dominate address activity, DeFi surpassed stablecoins in terms of transaction count, ending the quarter with an average of nearly 7 million transactions per day. TVL for revenue-generating protocols has steadily climbed from $26.5 billion in Q3'23 to $59.7 billion in Q1'24. This rebound indicates the return of confidence and liquidity in the DeFi market.

The Web3 gaming track has experienced significant growth, surpassing stablecoins in transaction volume and becoming the fastest growing Web3 year-on-year category. Compared with the fourth quarter of 2023, the daily active addresses of Web3 games in the first quarter of 24 increased by 155%, reaching a peak of 747,000. The number of transactions on the Web3 game track increased by 370% year-on-year.

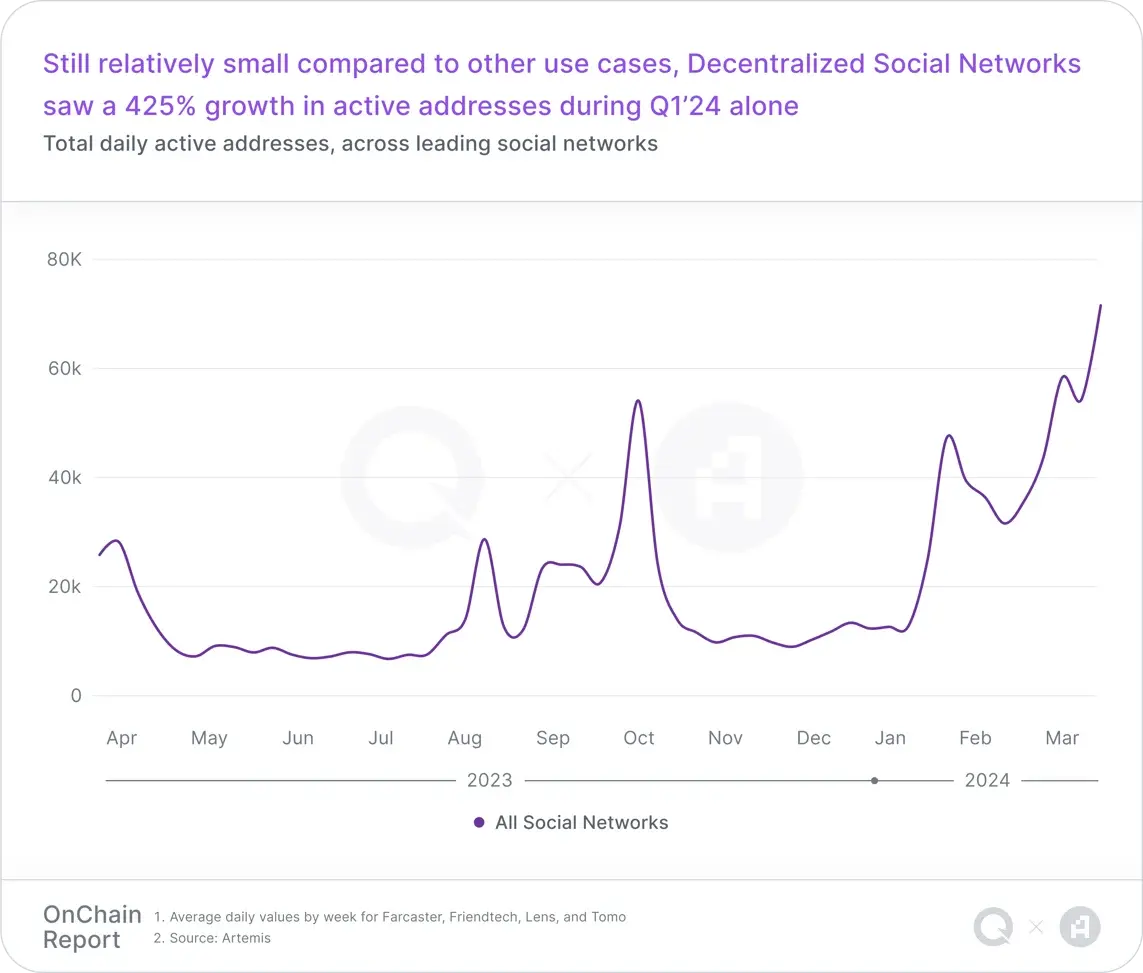

The decentralized social network experienced rapid growth in Q1’24, with a 425% increase in user activity, indicating The market is increasingly interested in blockchain-based social platforms, with mainstream platforms including Farcaster, Lens, friend.tech and Tomo.

Historically, the initial user engagement of decentralized social networks will decrease as the novelty of “uniqueness and novelty” gradually wears off. However, the gradual increase in the number of active users after the first quarter peak suggests that user engagement will be more stable over time, which may be a potential signal of increasing user acceptance.

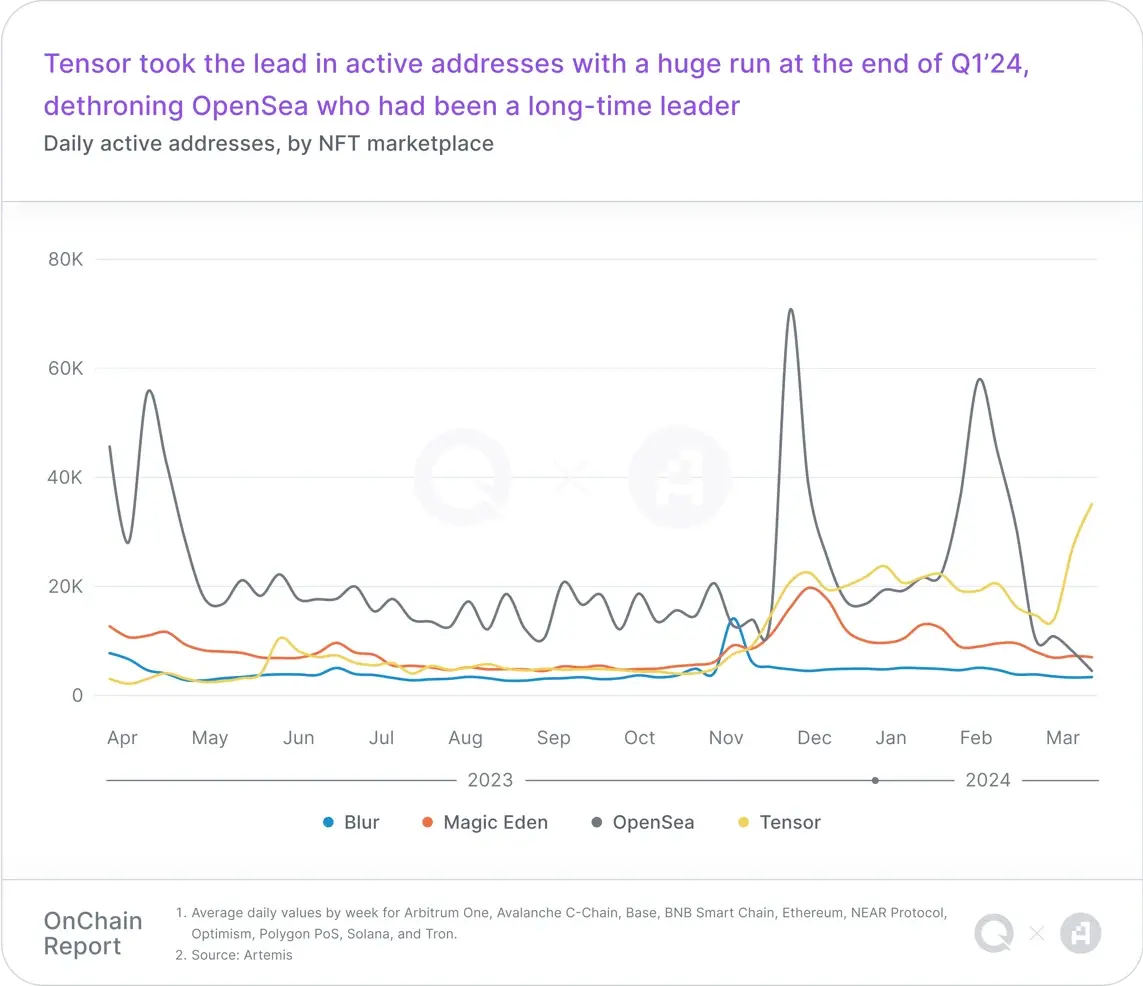

In 2023, Ethereum far exceeded other chains in terms of NFT market transaction volume, but in the first quarter of 24, Solana NFT market Transaction volume and activity surged. While OpenSea and Magic Eden have historically dominated the number of daily NFT active addresses and NFT transactions respectively, this trend was overtaken by Tensor in Q1’24, indicating changes in user preferences and platform performance.

Layer2 solution significantly improved the scalability of the blockchain in the first quarter of 2024, with faster transaction speed and more The low cost helps solve key challenges such as congestion and high transaction fees on major networks. The Layer 2 market continues to expand, with new chains launched every quarter.

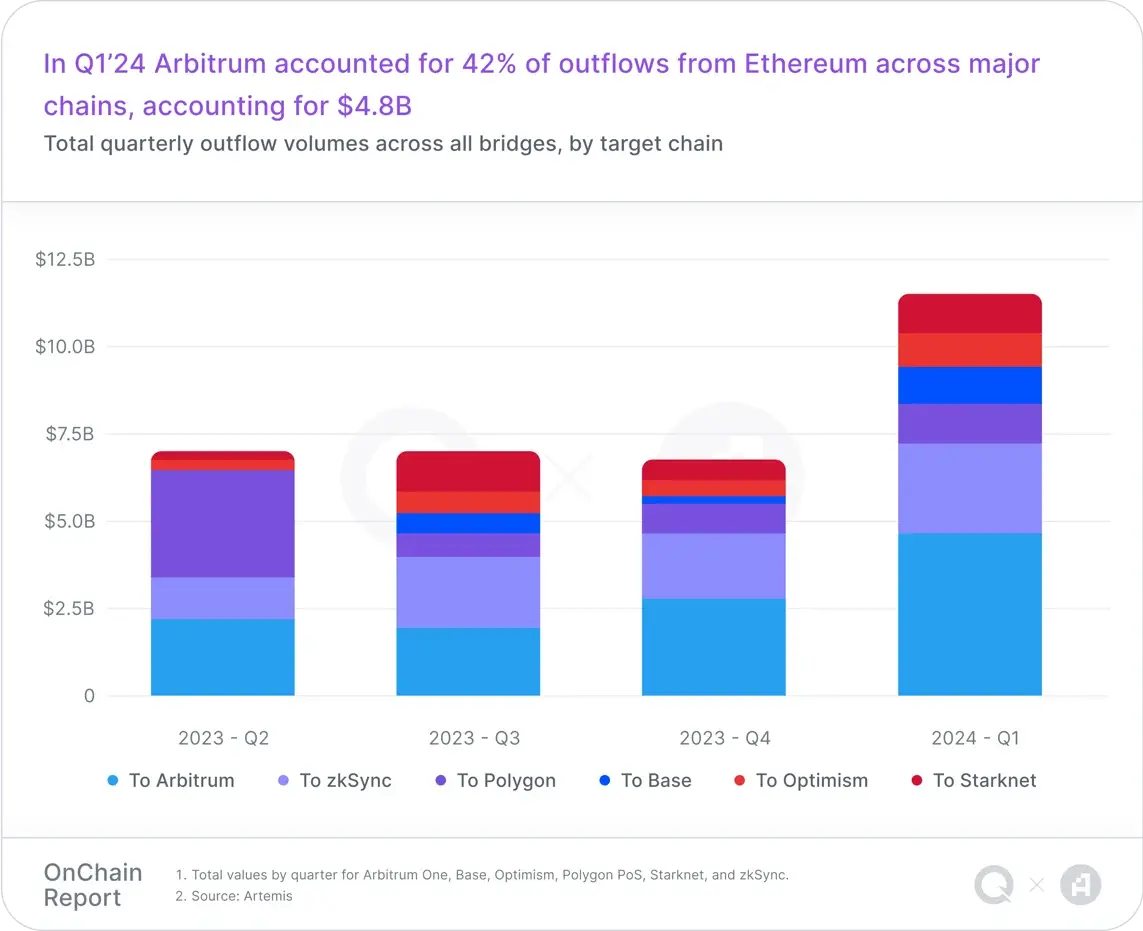

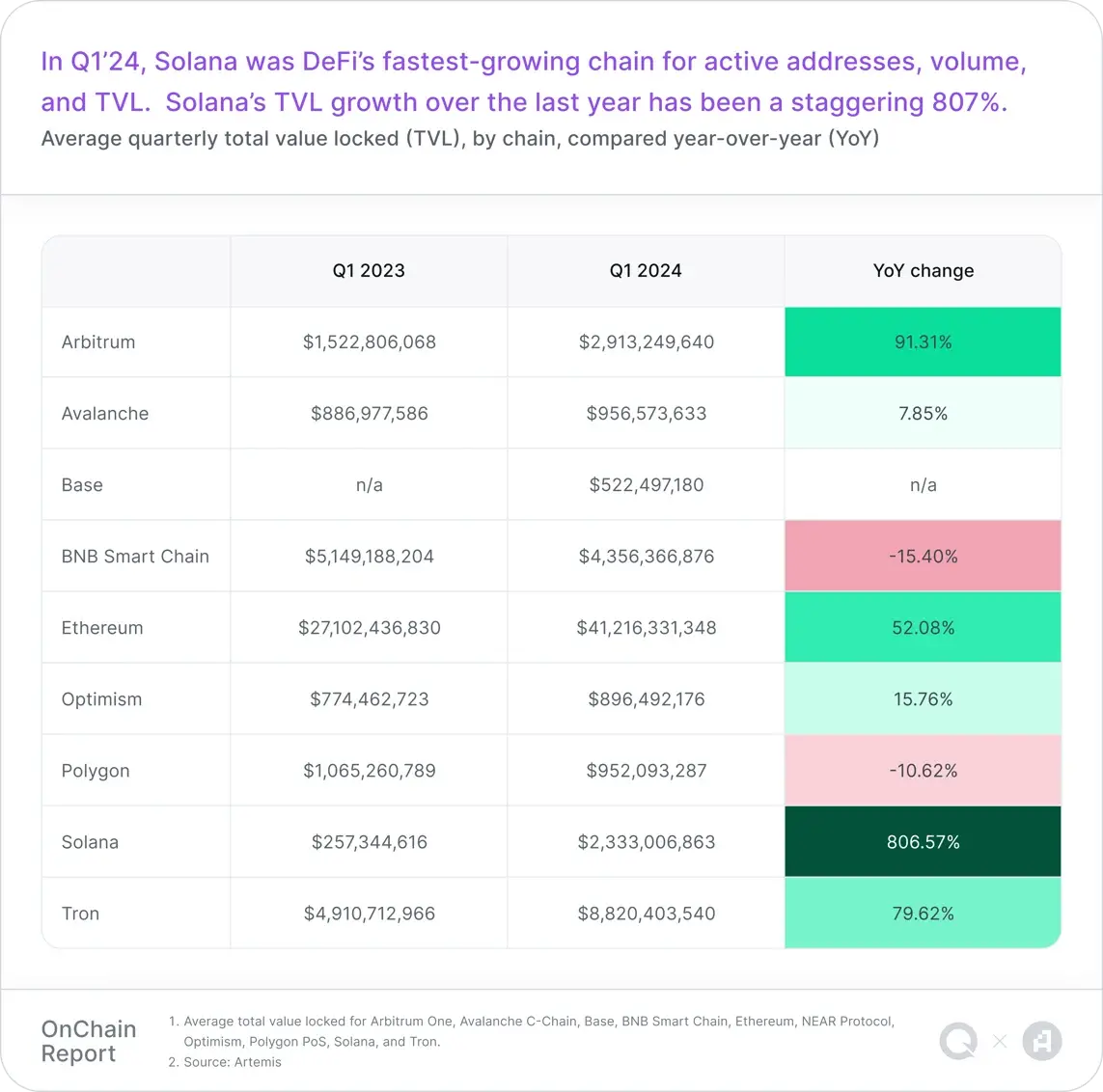

Despite fierce competition, Arbitrum has long been the L2 leader with 44% of TVL among all Ethereum Layer 2s .

During Q1’24, Arbitrum experienced two major events within a few days. The first event was the Dencun upgrade of the Ethereum network on March 13, which reduced L2 transaction fees by 98%. Artemis data shows that average daily transaction volume has almost doubled, growing by 96.2%, and average transaction fees have dropped by 93.5% (i.e. average Arbitrum transaction fees dropped from $0.3 to $0.01 almost overnight), but revenue has only dropped by 62.6%. In short, the Ethereum upgrade makes Arbitrum more suitable for mass-market applications.

The second event is the massive Arbitrum token unlocking on March 16th. With 1.1 billion ARB tokens worth $2.32 billion unlocked, the circulating supply of ARB tokens has almost doubled. After unlocking, ARB was sold by some whales (Note: According to Lookonchain monitoring, after large-scale unlocking, 11 whales deposited a total of 34 million ARB to the exchange, about 58 million U.S. dollars), and then large investors sold. Although Arbitrum The TVL has remained essentially unchanged, while daily active addresses and transaction volume have surged.

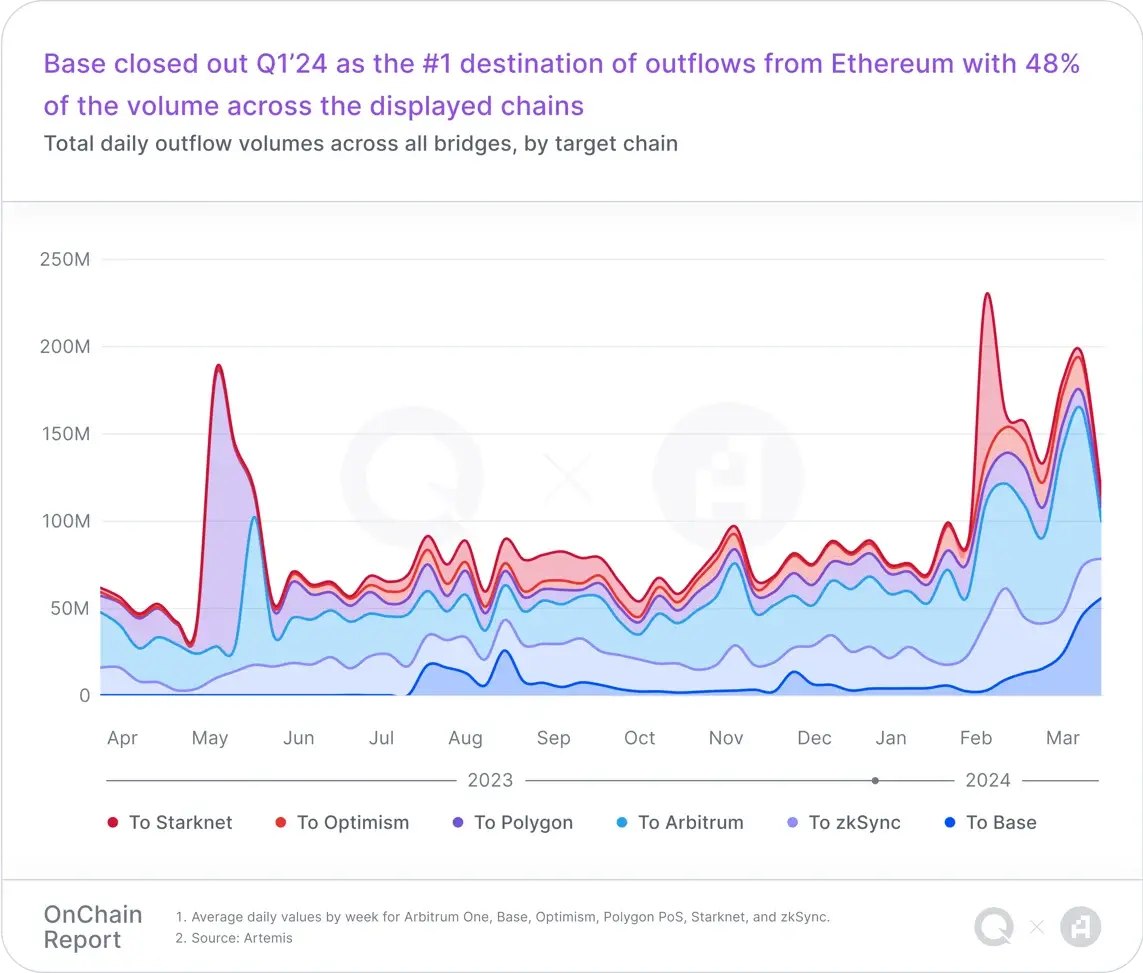

Coinbase’s new L2 network Base reached a major milestone in Q1’24 with TVL exceeding $1 billion. After the upgrade of Ethereum, the daily trading volume of DEX in the Base ecosystem reached its highest level ever in March, soaring 487%, and the daily trading volume exceeded US$1 billion for the first time.

Although Uniswap is Base’s largest DEX trading platform to date, Base has become a fertile ground for the development of emerging DEXs. Aerodrome, in particular, has become the second-ranked DEX in terms of transaction volume and TVL on the Base network. Base has also achieved tremendous growth in areas such as decentralized social applications. For example, Farcaster achieved great success in the first quarter. In addition, Memecoin is gradually being regarded by large ecosystems as one of the ways to attract new users and gain community attention.

Polygon released AggLayer v1 Mainnet on February 23, which introduced the aggregation layer (AggLayer). This cross-stack communication tool aims to unify fragmented blockchains into a network of ZK-secured L1 and L2 chains that feel like a single chain.

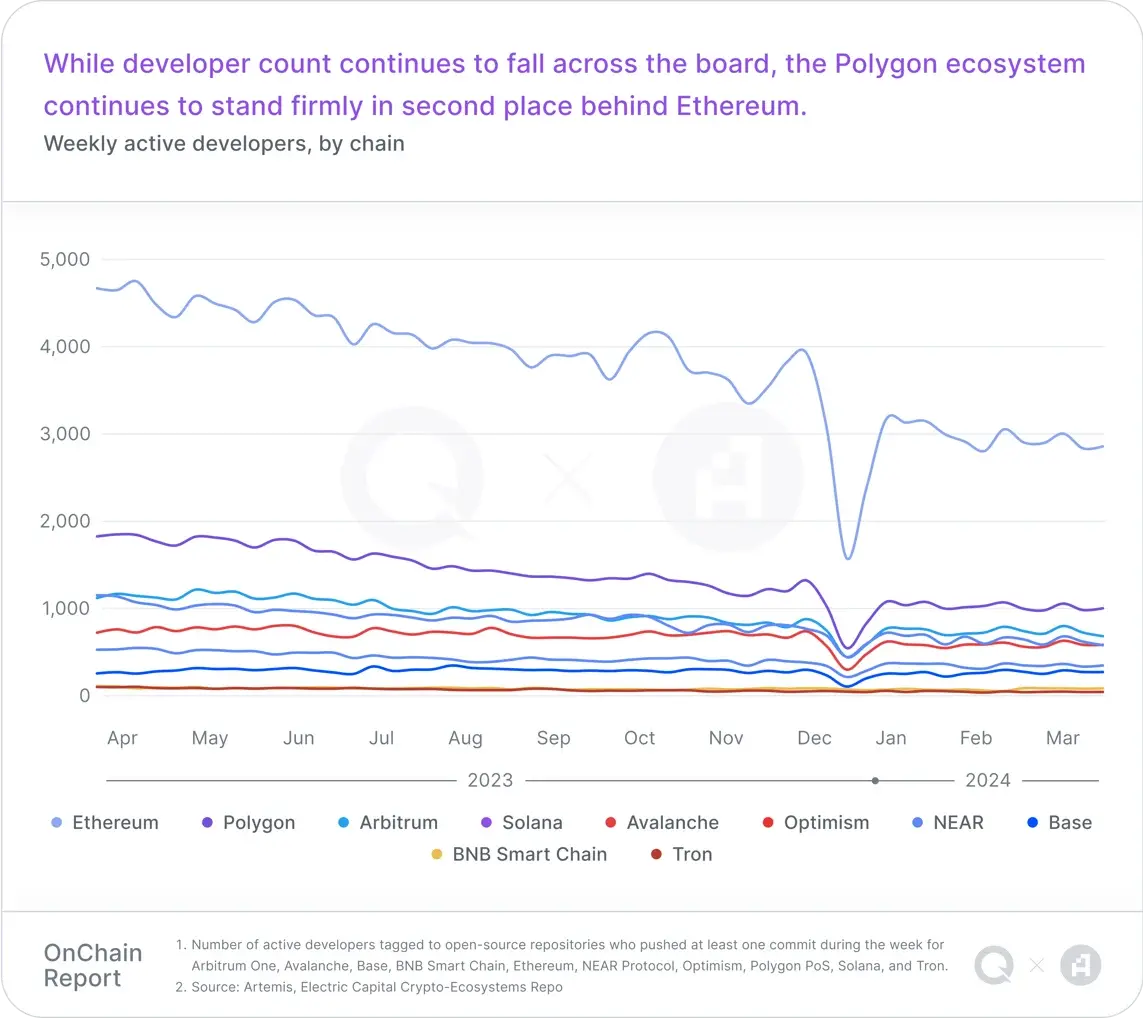

Additionally, Polygon is using its Chain Development Kit (CDK) to verify configurations transitioning from sidechains to L2 networks. Although Polygon's number of active developers continues to decline, it still maintains its second position.

In Q1’24, the Solana Foundation launched token extensions for stablecoin issuers such as GMO Trust and Paxos A range of configurable features. Solana has gradually become a paradise for retail investors, DeFi innovators, NFT minters, airdrop opportunists, and Memecoin traders in the first quarter of 2024. The influx of new address activity helped Solana’s average daily DEX trading volume increase by 180% month-on-month to $1.2 billion.

Solana revenue (in U.S. dollars) surged 597% quarter-on-quarter, from $7.1 million in the fourth quarter of 23 to $49.5 million in the first quarter of 24. The market value of the Solana ecosystem's stablecoins also increased by 49.4% month-on-month, from US$1.9 billion to US$2.9 billion.

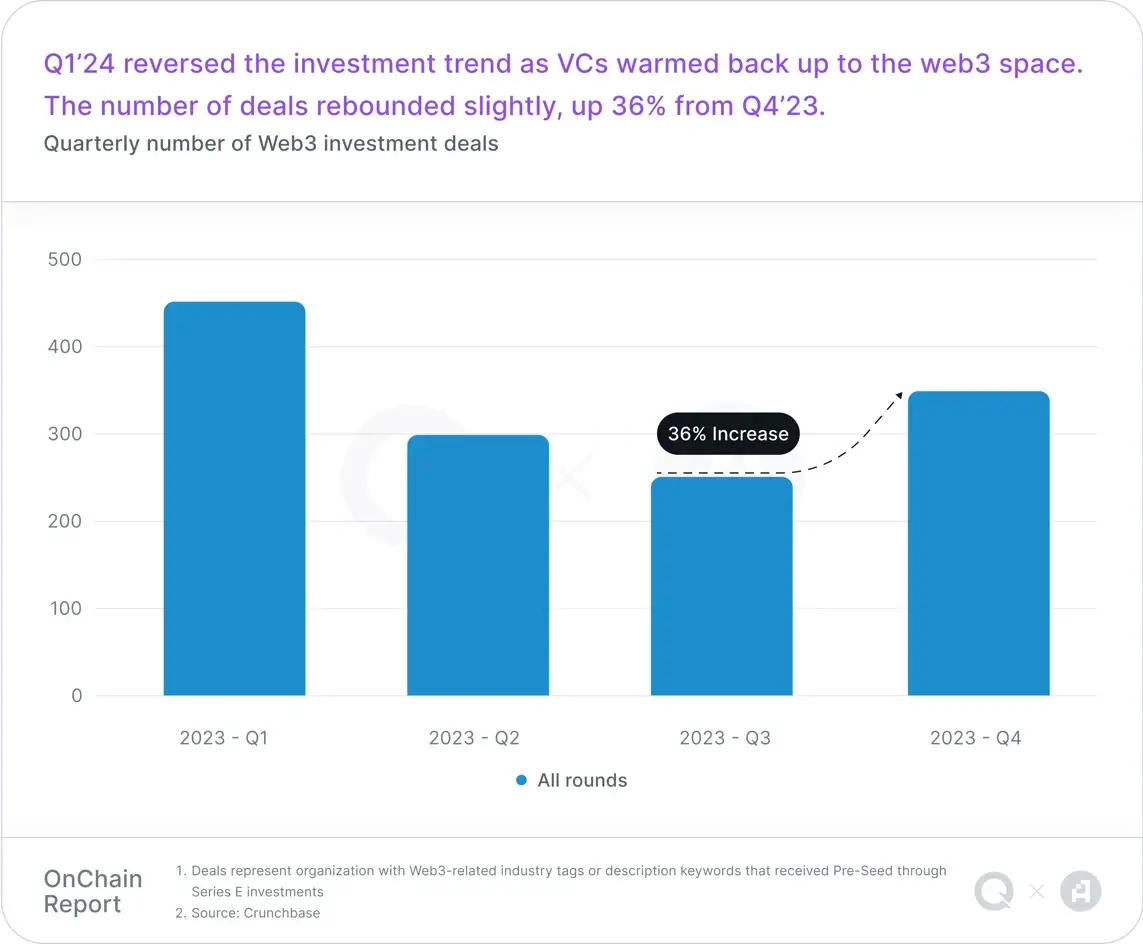

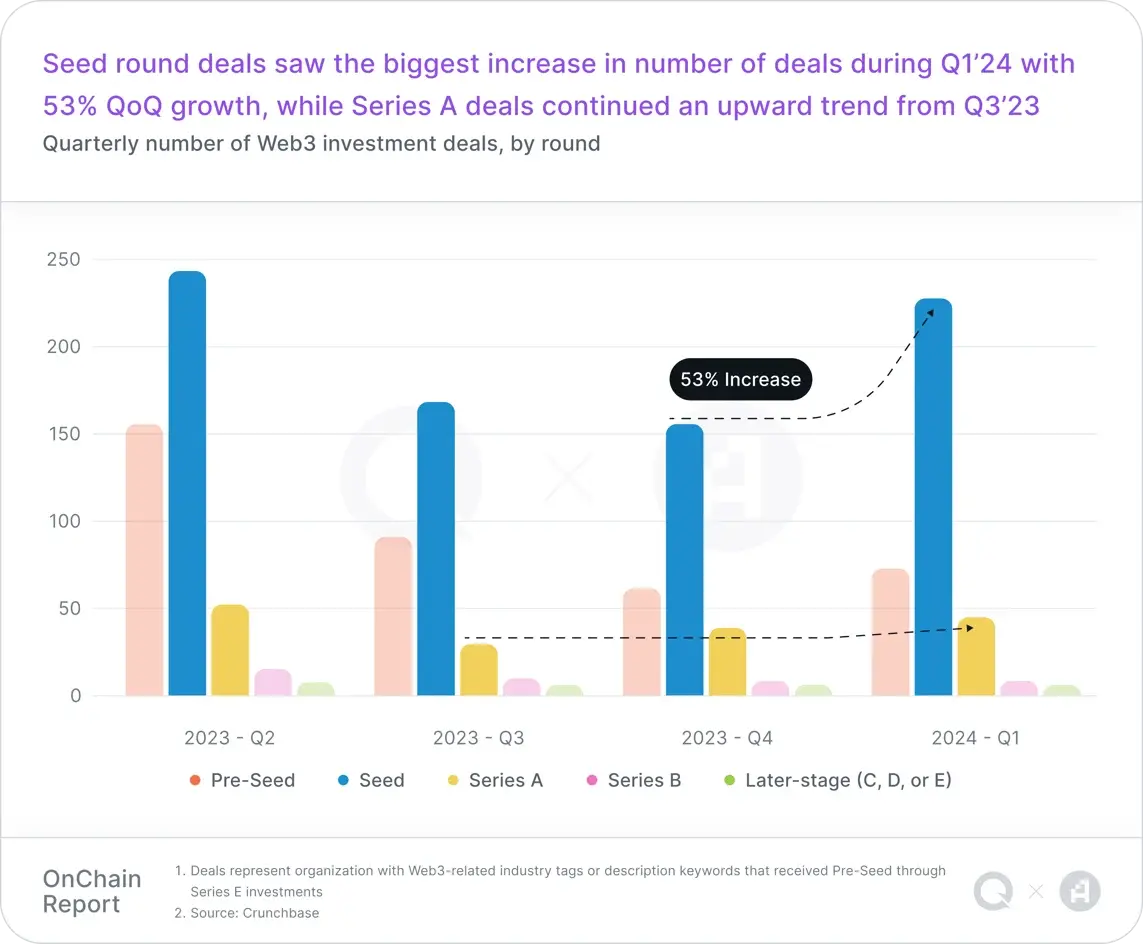

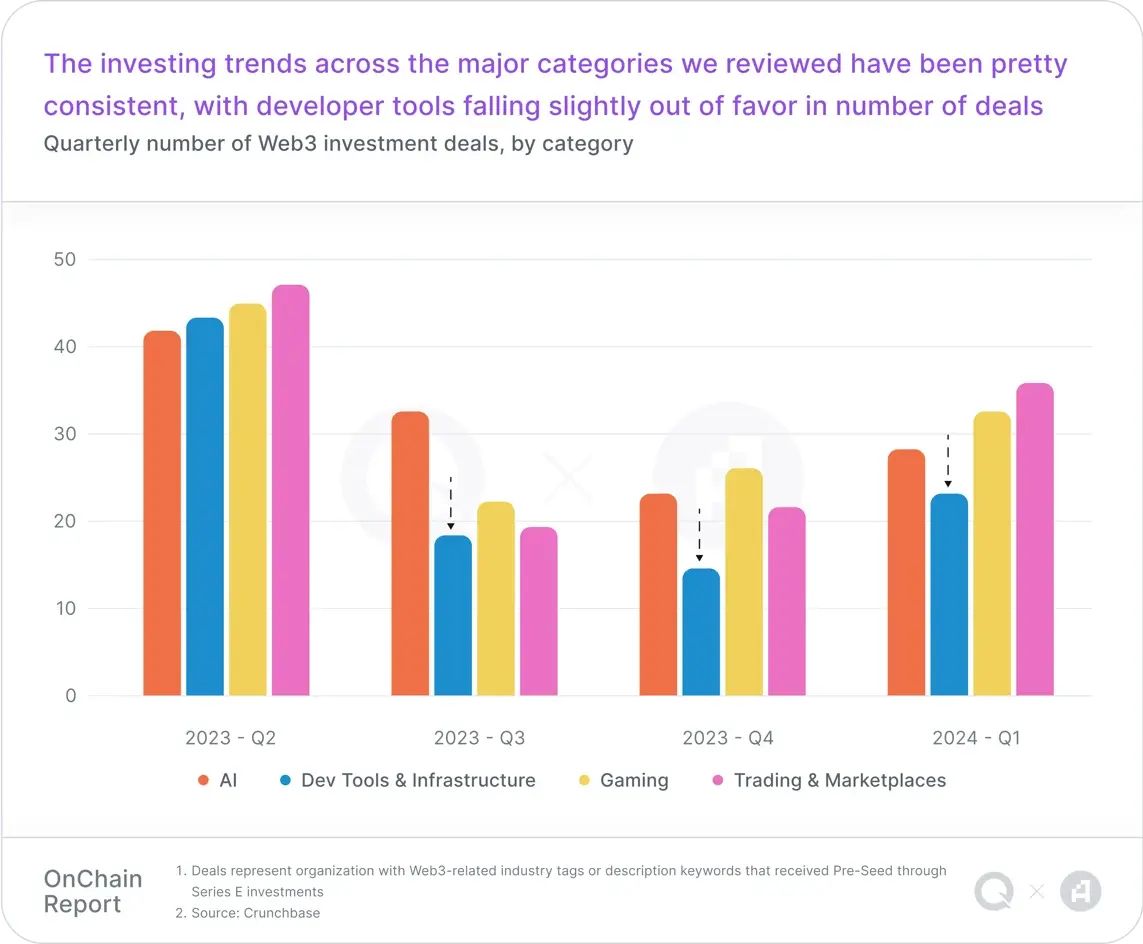

In addition to the 36% increase in the number of financings from the previous quarter, Web3’s total financing amount increased by 55% compared with the fourth quarter of 23. The number of seed round financing increased the most significantly, with a month-on-month increase of 53%. Series A and seed funding increased significantly, almost doubling the previous quarter. Among the funding categories, the field of AI was the most popular, demonstrating the market’s strong interest in exploring how AI can become a key value driver for Web3.

In contrast, areas such as developer tools and trading saw only modest increases in funding and volume, indicating a more cautious attitude among investors, possibly due to uncertainty or lower short-term returns in these areas.

Overall, growth in the Web3 VC market has resumed and highlights strategic shifts in the industry that VCs believe will have a significant impact and drive the evolution of the blockchain landscape.

The above is the detailed content of Q1 on-chain report: Layer 2 has expanded rapidly, and chain game users have grown significantly.. For more information, please follow other related articles on the PHP Chinese website!

![[Web front-end] Node.js quick start](https://img.php.cn/upload/course/000/000/067/662b5d34ba7c0227.png)